Still Working? Consider 12 Ways to Supercharge Your Retirement Savings

Save, save, save! You may feel like that’s all you hear when you’re researching how to plan for your retirement while you are still working.

It’s good, simple advice, but there is so much more to savings than to “just save more”. What accounts should you save to? What are the benefits of saving to one vs. the other? What tax implications should you be aware of? How much should you be saving?

In order to optimize your savings while you are still in the accumulation phase (i.e. working and still contributing to your investments), it’s essential to think through these types of questions so you can have the best plan tailored to your unique financial situation.

1. Build a Strong Financial Foundation

Before we dive deeper into optimizing your savings, it’s essential that you have a solid financial foundation in place. Although these suggestions may seem as basic as ABC, your personal finances are off to a strong start if you can check these three items off your list.

A) Maintain a stash of emergency savings

This might surprise you, but before you save for retirement, you should build up a stash of emergency savings. Emergency savings are the foundation of financial security.

An emergency fund, money typically held in easily accessible accounts like a high-yield online savings account or money market fund, is essential for dealing with unanticipated expenses or events such as a job loss, expensive home repair or large medical bill. As we all know, life is extremely unpredictable and things tend to pop up unexpectedly, so your emergency fund serves as a financial safety net to help navigate this uncertainty.

Learn more about how much you should have.

NOTE: You can earmark your emergency fund in the NewRetirement Planner as an account you don’t want to use as part of your withdrawal strategy in retirement. This can be done under My Plan > Accounts and Assets. If you have a specific savings account for emergencies only, you can hit the Pencil Edit icon and select ‘Yes’ for ‘Exclude this account from your withdrawal strategies?’

B) Get the FREE money, capture employer match

Employer match refers to a benefit offered by some employers wherein they contribute a certain amount of money to their employees’ retirement savings plans, such as a 401(k) or 403(b), sometimes it is based on the amount the employee contributes. The employer typically matches a percentage of the employee’s contributions, up to a certain limit.

Employer match is essentially free money.

You’ll want to understand how much your company matches your retirement contributions (if they match at all). Many companies typically match 100% of your own contribution, often up to a specified maximum percentage of your salary, which tends to be within the range of 3% to 6%. This matching formula will vary by plan so be sure to clarify with your employer.

It’s also super important to understand your company’s retirement plan vesting schedule. Generally, you’ll need to be at your company for about three years to be fully vested, meaning that money is yours if you decide to move on. This is also a plan-specific feature, so be sure to verify these details with your employer. Your own contributions, however? Those are yours, no matter what!

The key takeaway here is to aim to contribute enough to your workplace retirement plan to snag that full employer match.

NOTE: See the impact of an employer match by incorporating it into your NewRetirement Plan. Employer contributions to your retirement plan can be added under My Plan > Income > Work. You can also now add contributions your employer is making to your retirement plan regardless if you contribute or not (i.e. a non-elective contribution).

C) Pay off high-interest debts

Wait, paying off debt isn’t saving. True, but if you have emergency savings and are capturing employer match, your next priority really should be paying off high-interest debt.

When you’re investing in the stock market, nothing is a guarantee. Meanwhile, paying off high-interest rate debt, like a credit card for example, is a guaranteed investment return.

A guaranteed investment return means that when you put cash towards debt, your return is equal to the interest rate on that debt. So, when you use cash to pay off your credit card with an interest rate of 22%, you’re instantly earning a 22% investment return. Who doesn’t love a guaranteed return in the double digits?

The higher the interest rate on the debt, the more you save when you decrease your debt. Focus on paying off these costly debts with high interest rates before looking at optimizing your retirement savings.

2. Save AND Invest

It isn’t enough to just save. For everything but your emergency savings (which should be held in a liquid or easily accessible account), you will want to invest.

Investing allows you to take advantage of compounding returns. Your money will grow without any additional work from yourself.

3. Consider Following the Savings Playbook

Look, there is a lot to consider when it comes to saving. You have competing goals. To make it simple, start with the ABCs listed above and then proceed to knock off other savings goals, many of which are covered in more detail below.

4. Have a Solid Idea of How Much Retirement Savings You Are Going to Need

You’ve likely encountered various rules of thumb regarding retirement savings and needs:

- Save 15-20% of your gross income towards retirement, including any employer match

- Amass 25x your planned annual spending by retirement

- The 4% rule

Or perhaps you landed on an arbitrary number of $1,000,000, $3,000,000, or even $10,000,000? Maybe a friend or neighbor told you that’s what their “financial guy or gal” told them they need to have to retire.

The rules of thumbs are great starting points and simplify whether you are on track or not. But to answer the question for yourself, it pays to dig deeper.

There’s so many different variables to consider based on your unique situation:

- Did you start saving at 25 or at 40?

- Do you spend $5,000/month or $15,000/month?

- Are you invested in 100% bonds or 100% stocks?

- Do you anticipate an inheritance of $1,000,000 or none at all?

- Do you plan on working until 70 or want to stop completely at 50?

- Are you planning on retiring in California or Panama?

The good news is the NewRetirement Planner will allow you to plan step-by-step and show you how much savings you will need. By entering in your current and projected income sources, contributions and expenses, as well as assumptions like inflation and investment returns, you will gain peace of mind from seeing a detailed plan.

Take a lot of the guesswork out of it and make yourself a written plan. You won’t regret it!

5. Automate Your Savings

Autmating savings refers to the practice of setting up automatic transfers or contributions from your paycheck into your savings accounts.

Automating your savings is a good idea because it ensures:

- Consistency: By automating your savings, you ensure a regular savings habit, making it easier to achieve your financial goals over time.

- Discipline: Automation removes the temptation to spend the money earmarked for savings. Since the funds are transferred automatically before you have a chance to spend them, you’re less likely to dip into your savings for discretionary expenses.

- Goal Achievement: Regular contributions add up over time, helping you reach your targets faster.

6. Take Advantage of Different Tax Buckets

Now that we have the basics out of the way, it’s time to delve deeper into the many different types of accounts you may have access to as part of your retirement savings.

A) Know your tax buckets

You can think of taxable, tax-deferred and tax-exempt accounts as three “tax buckets”:

- Taxable accounts: Taxable accounts may include individual and joint brokerage accounts or trusts and do not have specific tax advantages.

- The money you put into a taxable account is after-tax money. After-tax money is money that has already been taxed and the remainder is available to spend or save.

- You also pay tax on the growth. Interest and dividends that your funds generate and any capital gains you realize, are taxable in the year in which they occur.

- Interest, non-qualified (ordinary) dividends and short-term capital gains are taxed at ordinary income rates while realized long-term capital gains and qualified dividends are taxed at preferential rates.

- Tax-deferred accounts: Tax-deferred accounts include traditional IRAs, 401(k)s and more. These savings vehicles give you immediate tax advantages.

- They are funded with pre-tax money. You invest your earnings without having to pay taxes on those funds.

- Growth is tax-deferred, which means you only pay taxes when you withdraw the money.

- Tax-exempt accounts: Tax-exempt accounts include Roth IRAs, Roth 401ks, and others. These accounts give you future tax advantages.

- They are funded with after-tax money, meaning money you have paid taxes on.

- Neither growth nor qualified distributions are taxed.

Now that you have a better understanding of how certain accounts fit into each tax bucket, let’s explore how you can maximize your savings potential using these various types of accounts.

B) Diversity Across Taxable, Tax-Deferred and Tax-Exempt Accounts

Of course, taxes are always important to keep in mind when you are making decisions about optimizing your savings. Maintaining a diversified portfolio of taxable, tax-deferred and tax-exempt accounts provides flexibility in how your withdrawals are taxed during retirement.

7. Get Triple-Tax Advantages with a Health Savings Account (HSA)

Once you have a fully funded emergency fund, paid off costly high-interest debt, and are taking advantage of your employer match, a Health Savings Account may be your next best option to optimize your retirement savings.

Most investment accounts fit neatly into one of the three tax buckets discussed above. However, the Health Savings Account is a unique account (in a good way!) that mixes some of the tax advantages of various buckets.

What is a Health Savings Account? A Health Savings Account (or HSA) is a type of savings account that is used to pay for eligible medical expenses. However, eligibility for opening an HSA isn’t open to everyone. To qualify, you must be enrolled in a high-deductible health insurance plan (HDHP) as defined by the IRS.

Contributions to an HSA are only permitted while you’re actively enrolled in a HDHP. However, even if you are no longer a part of a HDHP, you can still take advantage of any balance within the HSA and use the funds for qualified medical expenses.

Benefits of Funding an HSA: With an HSA, you have two primary paths for making contributions:

- Pre-tax payroll deductions through an employer

- Post-tax contributions to an HSA not tied to your employer and claiming a tax-deduction your tax return

Either way, you don’t pay any income tax on the dollars you contribute to your HSA (tax benefit #1!).

After you contribute to an HSA, you may want to invest those contributions for long-term growth if you plan on paying for ongoing medical costs out-of-pocket while working. With an HSA, you don’t pay any taxes on capital gains, dividends, or interest while holding or selling your investments (tax benefit #2!).

And when you withdraw money from the HSA to pay for qualified medical expenses, you don’t owe any taxes (tax benefit #3!).

Once you reach 65, you have the option to withdraw funds from the HSA without penalty, regardless of whether they are used for qualified medical expenses. However, withdrawals for non-medical expenses are still subject to income taxes, although the penalty of 20% that applies before age 65 is waived.

2024 Contribution Limits: For 2024, individuals under a high deductible health plan (HDHP) have an HSA contribution limit of $4,150.

The limit for family coverage is $8,300. If you are 55 or older, you can contribute an additional $1,000. These limits include any employer contributions as well.

8. Max Out Your Employer Retirement Plan Contributions

We discussed earlier how you should contribute enough to your employer retirement plan to get any employer match, but you don’t want to stop there!

Your next focus should be on increasing those contributions as much as possible until you hit the maximum for the year. A 1-2% increase in your contribution each year, or whenever you receive a raise, can pay huge dividends over the long-term.

9. Know Whether to Save in Pre-Tax or Roth

It’s never as simple as just making one type of contribution to your employer retirement plan, though. There’s options, of course.

Pre-tax vs. Roth contributions

For many individuals, you may have a 401(k) or a 403(b) plan through your employer.

For these types of plans, you often have the option to contribute on a pre-tax basis and/or a Roth basis. The difference in contributions are as follows:

- Pre-tax: tax deduction when you contribute, pay taxes when you withdraw later in retirement

- Roth: no tax deduction when you contribute, but qualified distributions are tax-free in retirement

When thinking through whether to make pre-tax or Roth contributions:

- Contribute on a pre-tax basis: you believe you will be in a lower tax bracket when withdrawing money in retirement vs. now

- Contribute on a Roth basis: you believe you will be in a higher tax bracket when withdrawing money in retirement vs. now

Given we don’t know what the future holds exactly for tax legislation, brackets and rates, deciding whether it makes sense to make pre-tax or Roth contributions can be difficult. However, it doesn’t have to be an either/or decision. You can do both, as well (assuming your plan permits Roth contributions)!

NOTE: You can model making pre-tax, Roth or a mix of pre-tax and Roth contributions in the NewRetirement Planner to see the impact on your long-term financial plan.

After-tax contributions

Your employer plan may also offer the ability to make after-tax contributions.

Generally, after-tax contributions are a consideration after maxing out your pre-tax and/or Roth contributions for the year.

While you won’t get a tax deduction for an after-tax contribution, contributions are tax-free at withdrawal, but any earnings generated on those contributions are taxed as ordinary income at the time of distribution.

With money in an after-tax account, your plan may also permit you to take advantage of a Mega backdoor Roth strategy.

A mega backdoor Roth strategy is when, after making after-tax contributions, you convert the contributions immediately to a Roth 401(k) or Roth IRA. This way, both the after-tax contributions and the earnings would be tax-free in retirement, vs. just the contributions (when making after-tax contributions and leaving them as is).

Confirm with your HR department to ensure you can implement this type of strategy because your plan has to offer either in-service (while working) distributions to a Roth IRA or the ability to move money from the after-tax portion of your plan into the Roth 401(k) part of the plan (if there is one).

2024 contribution limits

For 2024, the limit for pre-tax and/or Roth contributions to 401ks, 403bs, most 457s as well as Thrift Savings Plans is $23,000. And, if you are 50 or older, the catch-up contribution is an additional $7,500. So, you can save a total of $30,500!

If your employer retirement plan allows for after-tax contributions, the maximum that you and your employer combined can put into your plan is $69,000, or $76,500 for individuals 50 and older in 2024.

10. You Aren’t Limited to Employer Savings: Max Your Savings Outside of Your Employer

Not all of your retirement savings have to be through your employer plans. Along with an employer retirement plan or a Health Savings Account, you may also have an IRA or taxable brokerage account that can play a significant role in your annual savings plan.

Traditional IRA

When you make a contribution to a traditional IRA, you have the potential to receive a tax deduction on your contribution, your money grows tax-deferred, and distributions from the account will be hit with ordinary income tax. The maximum you can contribute to an IRA (Traditional or Roth) in 2024 is $7,000 ($8,000 for individuals 50 or older).

There are, however, limits on the deductibility of IRA contributions. If during the year either you or your spouse was covered by a retirement plan at work, the deduction may be reduced, or phased out, until it is eliminated, depending on filing status and income:

- Single Filers: Modified Adjusted Gross Income (MAGI) between $77,000 and $87,000

- Married Filing Jointly: if the spouse making the IRA contribution is covered by a workplace retirement plan, MAGI between $123,000 and $143,000

- Married Filing Jointly (IRA contributor is not covered by workplace retirement plan but spouse is): MAGI between $230,000 and $240,000

- Married Filing Separately: MAGI between $0 and $10,000.

If neither you nor your spouse is covered by a retirement plan at work, the phase-outs of the deduction do not apply.

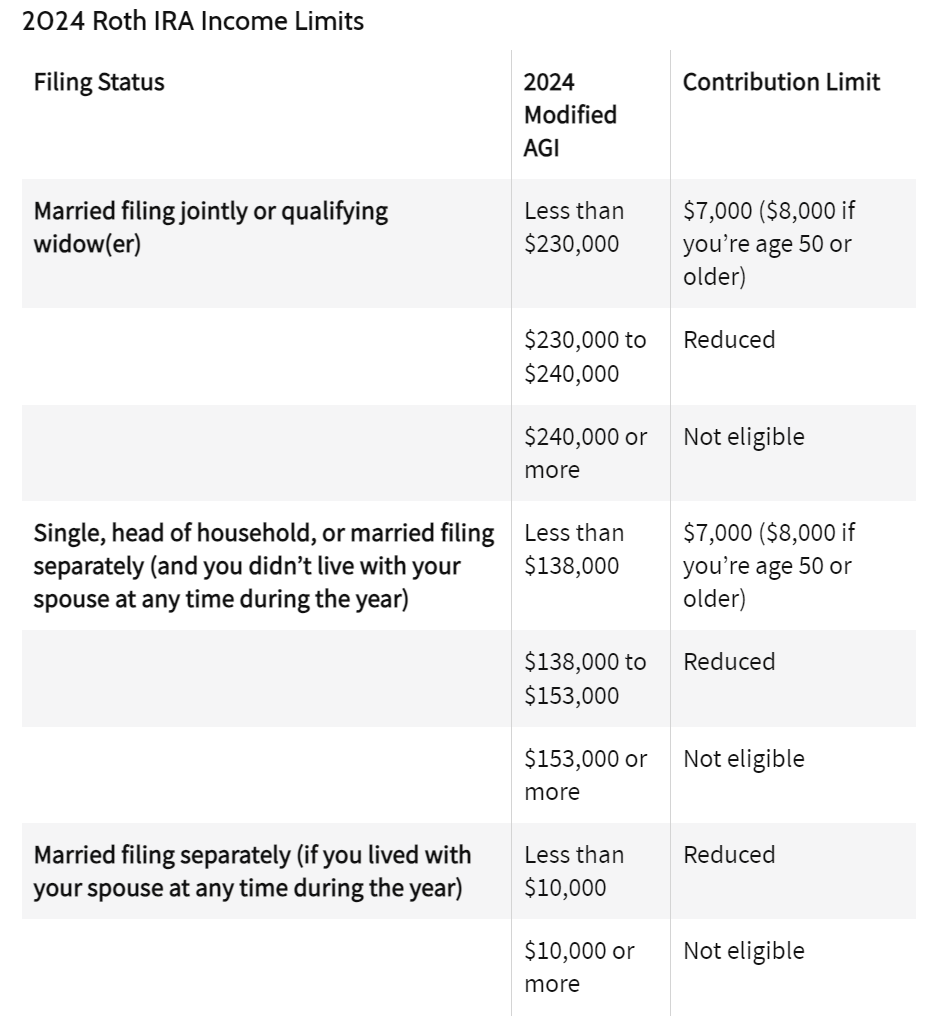

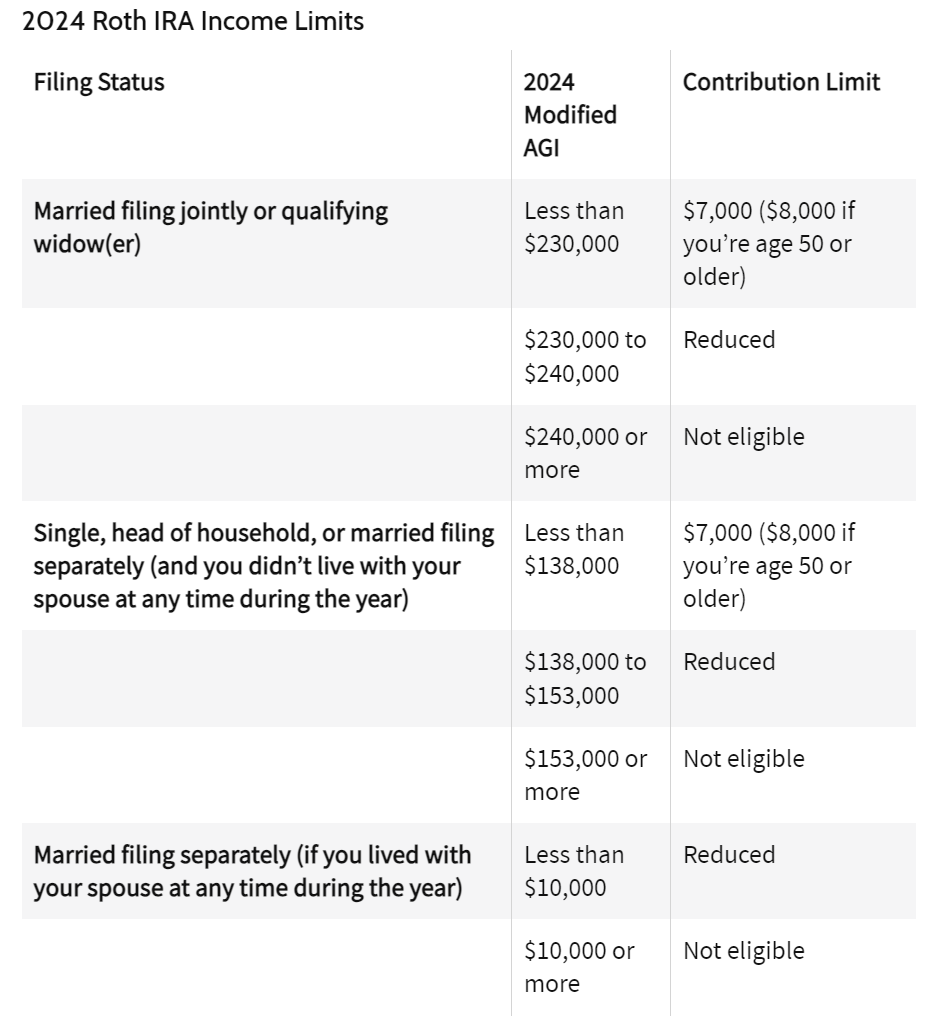

Roth IRA

When you make a contribution to a Roth IRA, you are putting money into the account after paying income tax on it, and then those dollars grow tax-free and can be withdrawn tax-free.

However, there are income limits that restrict who can contribute directly to a Roth IRA:

11. Consider a Backdoor Roth IRA Strategy

If you earn too much to contribute directly to a Roth IRA, given the income limits above, you may consider a backdoor Roth IRA strategy.

This involves making a non-deductible Traditional IRA contribution and then making a subsequent conversion to a Roth IRA account.

However, before considering this strategy, you’ll want to be aware of the IRS’ pro-rata rule. This rule requires you to consider ALL of your IRAs as the same account. Therefore, if you have a Traditional IRA, SIMPLE IRA or SEP IRA, those balances are considered when it comes to determining your tax owed on the conversion. So, if you have a balance in any of these types of accounts at the end of the year, you may want to reconsider a backdoor Roth IRA strategy.

Taxable Accounts

After exhausting your tax-advantaged accounts above, as a high earner or super-saver, you may consider a taxable account, like an individual or joint brokerage account, next.

Taxable brokerage accounts do offer a lot of flexibility in that there are no contribution or income limits like most of the accounts we’ve discussed up until now. You can also sell and take the money whenever you need to!

While taxes on dividends and capital gains are inevitable each year, adopting a low-cost, hands-off investment strategy can still mean relatively minimal taxes and foster long-term growth on your contributions.

NOTE: Considering tax mitigation strategies such as asset location and tax loss-harvesting is essential when investing in taxable accounts.

12. Build and Maintain a Holistic Financial Plan

It is likely that you try to eat well, exercise regularly, socialize with friends, and work, read books, or engage in other activities that keep your brain working well. These are all activities related to “wellness.”

But, do you also have habits and a practice around your financial life? Personal finance is a critical component of your overall well being. Building and maintaining a personal financial plan for all aspects of your money is a great first step to taking control of your financial life.

Use the NewRetirement Planner to take control and build the habits you need for better financial decisions, confidence, security, and peace of mind.